7 Financial Tips for Business Owners During COVID-19

Following the recent restrictions on gatherings, businesses that are allowed to be open, and all other health concerns and restrictions, your business may be caught in the wake of COVID-19. You are not alone. There are many business owners in similar positions to yours. While I don’t have a silver bullet for ending this pandemic (unfortunately) I do have a couple ideas of how you and your business can move through this turbulent time.

Be Proactive With Creditors and Landlords

For many people, rent and mortgage payments are due on the first of April, coming up in ten days. You may also have other bills, such as credit cards or debt payments coming up soon. If you are at all concerned about your ability to make these payments, I encourage you to get in touch with your creditors and/or landlords. Politely but firmly explain your situation to them and ask if you can work something out, like a reduced payment or a refined payment schedule. Because so many people are in a similar place, you may garner their sympathy and receive some assistance.

Cull Your Expenses

Now is the time to really go through your personal and business expenses with a fine-tooth comb. Cancel any subscriptions or memberships that aren’t vital. If you’re in California or Illinois, for example, then you’re probably not going to the gym or yoga studio anytime soon. Review your business’s spending needs and nix anything unnecessary or now irrelevant.

Get Creative With Your Services

Think about ways you can adapt your business to the current times. Maybe it’s time to ramp up your online store and start doing local delivery. Many yoga teachers and entertainers are starting to offer their services online. Brainstorm and get creative.

Check Available Resources

Every community has different resources available to those struggling with expenses due to COVID-19. Here in California, you can refer to the information provided by the Employment Development Department to see if you qualify for aid. Also check local nonprofits and other resources. Many communities are creating volunteer networks and community funds to protect the most vulnerable in the community. If you are seriously at risk, consider seeking these out. Otherwise, consider contributing to them, either monetarily or with volunteer time.

Lean On Your Money Team

This is a time when those on your money team can really come in handy. Reach out to your financial confidants, your bookkeeper, financial coach, etc. and start strategizing on how you can fortify your business during these tough times. Don’t make these decisions alone; remember that you have allies.

Mindset Matters

Although the virus is seriously threatening, those most at risk are the elderly and the immunocompromised. It’s important to remember that we are taking all of these measures in the name of collective care, to protect those of us who are most vulnerable. I encourage you to remember this and to avoid self-victimizing, panicking, or hoarding. Holding onto a mindset of courage and generosity will do wonders in this time, for your own mental health and everyone around you.

File Your Taxes On-Time!

File Your Taxes On-Time!

You may have heard that the IRS has officially extended the deadline to pay taxes to July 15, 2020. While this is great news for business owners, it’s important to remember that you still need to file your taxes by April 15th. If you are unable to meet this deadline, you can request a six-month extension for filing. You can check out the IRS site for more info. EDIT: The deadline to file has also been extended!

I hope these ideas bring you some sense of hope and agency in unpredictable times.

Angela

#4 – You should have received all of your tax mailings by mid-February. If your tax preparer is going to want everything in electronic form (or you just want to stay super organized) scan all of your paper statements and add them to your 2017 Tax Documents folder.

#4 – You should have received all of your tax mailings by mid-February. If your tax preparer is going to want everything in electronic form (or you just want to stay super organized) scan all of your paper statements and add them to your 2017 Tax Documents folder.

What Do You Gain From This?

What Do You Gain From This?

So, what do you gain when your records are well-kept? Errors are corrected, which can potentially save you money right out the gate. You incur no late fees on taxes because everything is organized and filed on time. You can use your reliable records to glean insights into when and how money is made in your business. You have less stress about finances because you know everything is being tracked correctly. And finally, you have more time to do the things in your business that you actually enjoy. Should you be spending your time doing bookkeeping when you’re actually really fabulous at making art, building cabinets, providing live entertainment, etc?

So, what do you gain when your records are well-kept? Errors are corrected, which can potentially save you money right out the gate. You incur no late fees on taxes because everything is organized and filed on time. You can use your reliable records to glean insights into when and how money is made in your business. You have less stress about finances because you know everything is being tracked correctly. And finally, you have more time to do the things in your business that you actually enjoy. Should you be spending your time doing bookkeeping when you’re actually really fabulous at making art, building cabinets, providing live entertainment, etc?

Earlier in this article, I mentioned that a financial planner can be a good reference, but another option is to simply meet with a planner at a firm as needed. I had one client who, when planning for retirement, made one appointment at a firm and got all her questions answered. No commitment needed, and a good source of advice.

Earlier in this article, I mentioned that a financial planner can be a good reference, but another option is to simply meet with a planner at a firm as needed. I had one client who, when planning for retirement, made one appointment at a firm and got all her questions answered. No commitment needed, and a good source of advice.

Making a regular habit of checking in with your finances. Make this easy by consolidating your passwords to your different accounts and portals. If you don’t have to go searching for passwords before you begin your checkin, you’re way more likely to actually do it!

Making a regular habit of checking in with your finances. Make this easy by consolidating your passwords to your different accounts and portals. If you don’t have to go searching for passwords before you begin your checkin, you’re way more likely to actually do it!

If you enjoyed this guide, I recommend also checking out

If you enjoyed this guide, I recommend also checking out

The Function of Profit

The Function of Profit

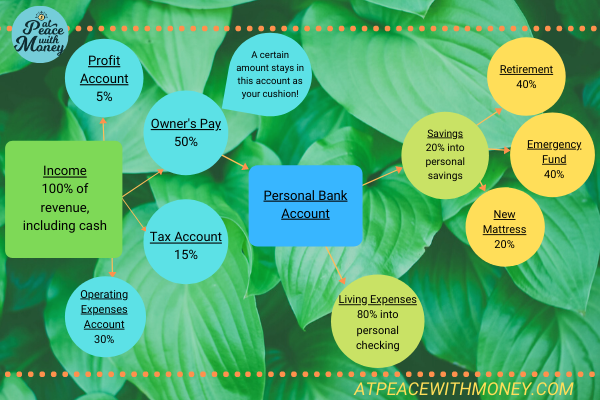

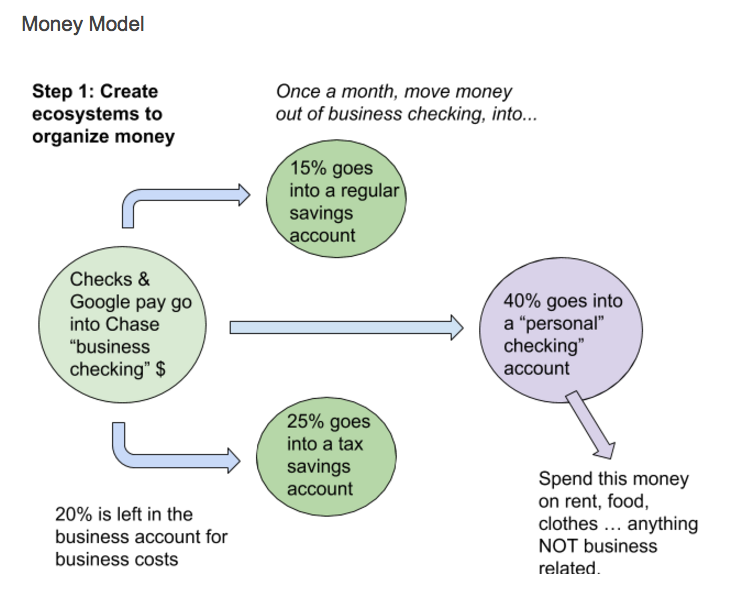

Above all, the goal of money mapping is to know where your money is going every step of the way. From the moment you receive income, to the moment that money is saved for taxes, invested for retirement, or put away for a savings goal – you’ve got a plan. Consequently, this is an opportunity to define those final destinations. Creating a tax savings account and an operating expenses account come in handy here. You can also think about creating savings goals for yourself, and making a plan to contribute regularly to those.

Above all, the goal of money mapping is to know where your money is going every step of the way. From the moment you receive income, to the moment that money is saved for taxes, invested for retirement, or put away for a savings goal – you’ve got a plan. Consequently, this is an opportunity to define those final destinations. Creating a tax savings account and an operating expenses account come in handy here. You can also think about creating savings goals for yourself, and making a plan to contribute regularly to those.

Doing some emotional work around money can also really help you clear up your oversaving. I recommend reading

Doing some emotional work around money can also really help you clear up your oversaving. I recommend reading