How to Get the Best Financial Advice: Build a Financial Advice Team

Money is a team sport. Although we have an unfortunate notion in our culture that talking about money is taboo, we need to do our best to break it. By collaborating with others and building a team of people we can trust to talk to about our money, we can start getting the help and information we need.

There are many different people who can make up a money team. Money confidants, such as close friends and coaches who you can confess your financial feelings to, and receive good advice from, are one good example. Your bank can be considered a part of your money team, especially because good customer service is an important aspect of banking. Similarly, your tax prep person, financial planner, accountant or bookkeeper, and even the people you get financial advice from, are all important parts of your money team.

These “team members” fall into three different categories: people in your life, trusted professionals, and advice sources. Let’s take a look at each category and figure out how you can find good team members.

People in Your Life

Anyone in your life who you’re able to talk to about money falls here. Most importantly, these people are able to provide you with space to air your feelings. In some cases, they may also offer good advice. For example, if you’re friends with an accountant or a retirement planner, you’ve hit the jackpot! If not, good friends that you can open up to are still very helpful. The more we air our feelings about money, the more we’re able to think clearly and pursue practical solutions

If you don’t have anyone in your life that you’d consider a financial confidant, don’t worry. Run through your list of connections and identify some people with whom you might feel safe sharing thoughts, feelings, and ideas about money. Then, try approaching them with the idea of sharing these things. Many people are happy to have someone to talk to about this, so it’s worth a shot. For more tips, you can read my article on “Why You Need a Money Buddy.”

Trusted Professionals

Here’s where your team members might get more diverse. Financial coaches, bookkeepers, tax preparers, and financial planners all fall into this category. Not everyone will need to refer to every one of these professionals, and perhaps not on a regular basis. However, working with professionals in all of these areas can do wonders for your financial life.

Like a money buddy, coaches are there for you to confide in, but are also trained to help you find specific solutions. Good bookkeepers are able to deliver valuable financial insights about your business and follow appropriate record-keeping laws. If you run a business, you might find you appreciate that someone else does your record keeping, while you get to do whatever it is you really enjoy. Here’s an article about how to find a good bookkeeper.

Tax preparers are great to consult with during tax season. The most helpful tax preparers help you get a better idea of what you need to file, what you can write off, and if you qualify for any credits. Depending on your assets, you may or may not need to have a financial planner you can regularly work with. If you want to do some complex planning, it might be good to consider adding a financial planner to your money team.

Advice Sources

The last category is made up of public figures and advising entities. Your bank is probably the most important member of your money team here. If you don’t have a bank that provides good customer service, or if you’re getting charged bank fees, switch, and fast. Being able to sit down with a bank employee when you have questions is an important aspect of building your money team. Bank fees are just annoying, but also totally avoidable! Read my articles about “How to Avoid Bank Fees” and “How I Broke Up With Wells Fargo (And You Can Too!).”

Earlier in this article, I mentioned that a financial planner can be a good reference, but another option is to simply meet with a planner at a firm as needed. I had one client who, when planning for retirement, made one appointment at a firm and got all her questions answered. No commitment needed, and a good source of advice.

The last member of this category is public advice figures. There are quite a few out there, so finding the ones who give the best advice for you might require some sifting. These articles contain some of my thoughts on finding good financial advice. Also, here are a couple of my personal favorite resources.

Building a money team takes some work, but when you have a network of people, professionals, and resources who can help you solve your money problems, you’ll be glad you did it! If you enjoyed this article, you might like my free e-Book, 9 Secrets of Financial Self Care. Click here or below to get your copy!

If you’ve spent much time in the business coaching sphere looking for advice, you may have come across someone’s ad inviting you to work with them to “Have your first 25k month!” (or whatever the promise is). While these nice round numbers might sound nice, they’re really there for the slogan, not for you.

If you’ve spent much time in the business coaching sphere looking for advice, you may have come across someone’s ad inviting you to work with them to “Have your first 25k month!” (or whatever the promise is). While these nice round numbers might sound nice, they’re really there for the slogan, not for you.

Earlier in this article, I mentioned that a financial planner can be a good reference, but another option is to simply meet with a planner at a firm as needed. I had one client who, when planning for retirement, made one appointment at a firm and got all her questions answered. No commitment needed, and a good source of advice.

Earlier in this article, I mentioned that a financial planner can be a good reference, but another option is to simply meet with a planner at a firm as needed. I had one client who, when planning for retirement, made one appointment at a firm and got all her questions answered. No commitment needed, and a good source of advice.

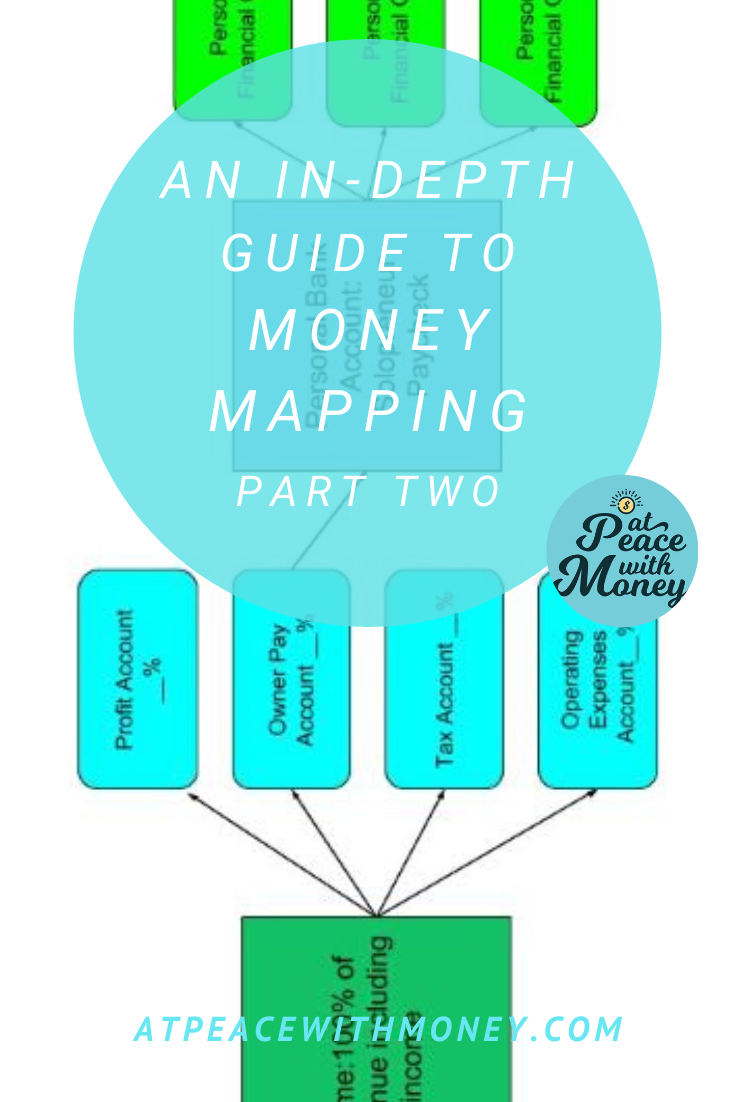

The Function of Profit

The Function of Profit

Above all, the goal of money mapping is to know where your money is going every step of the way. From the moment you receive income, to the moment that money is saved for taxes, invested for retirement, or put away for a savings goal – you’ve got a plan. Consequently, this is an opportunity to define those final destinations. Creating a tax savings account and an operating expenses account come in handy here. You can also think about creating savings goals for yourself, and making a plan to contribute regularly to those.

Above all, the goal of money mapping is to know where your money is going every step of the way. From the moment you receive income, to the moment that money is saved for taxes, invested for retirement, or put away for a savings goal – you’ve got a plan. Consequently, this is an opportunity to define those final destinations. Creating a tax savings account and an operating expenses account come in handy here. You can also think about creating savings goals for yourself, and making a plan to contribute regularly to those.

If a resource ticks all these boxes for you, it will probably set you down the path to financial wellbeing! And it will feel a lot better than trying to read something that just isn’t for you. Next time, we’ll talk about starting the search for resources. For now, feel free to do some good ol’ googling. You can also check out my article on

If a resource ticks all these boxes for you, it will probably set you down the path to financial wellbeing! And it will feel a lot better than trying to read something that just isn’t for you. Next time, we’ll talk about starting the search for resources. For now, feel free to do some good ol’ googling. You can also check out my article on